🕹The Biggest Fintech Acquisition in India

Four point seven billion dollars

This week was pretty big for Indian fintech: a fintech company called PayU acquired another fintech company called Billdesk for $4.7 billion. This is the biggest ever fintech acquisition in India.

Look, I know Indian fintech is booming and lots of fintech startups are getting lots of funding.

But this acquisition is still shocking.

I mean, $4.7 billion dollars???!!!!

That’s why I decided to deep dive into this acquisition and understand why PayU paid such a huge price for Billdesk.

In today’s article, I'll start the story from PayU, then explain about Billdesk, and then finally explain why this acquisition and why the price makes sense.

Let's go🚀🚀

🕹From South Africa to China to The Netherlands to India:

Before 2001, Naspers was just a boring TV company in South Africa.

But in 2001, they paid $34 million to get a 46.5% stake in a small Chinese startup. Today, that startup is a $600 billion tech giant called Tencent. And Naspers' stake in Tencent is worth $200 billion!! Naspers became a tech giant overnight.

(Does this story sound familiar? It's because Softbank, one of the biggest tech investors in the world, had a similar story. They also invested in a small Chinese startup which later became a tech giant called Alibaba. And Softbank became a huge investment company overnight)

This was the smartest investment by Naspers, maybe one of the smartest investments in the history of investments.

Due to its stake in Tencent, Naspers became so big that the South Africa stock exchange couldn't handle it. So Naspers created a subsidiary company in The Netherlands called Prosus. And Naspers unloaded its entire Tencent stake along with all its international investments to Prosus.

(does the name Prosus ring a bell? Maybe that's because they acquired Stack Overflow last month for $1.8 billion)

Armed with this giant money bag, Prosus, had one mission(should they choose to accept it)- find the next Tencent. That's what Prosus does: it finds and invests in companies and markets which have huge potential.

After reading this, you may think that Prosus is a VC. But there are some big differences between the 2. Prosus isn't like a traditional VC: they don't operate a fund, don't take money from outside investors, and don't have a limit on how much or how long to invest in a company.

In India, Prosus has invested in companies like Byju's, Swiggy, OLX, Meesho, etc.

Prosus' first investment in India was a startup called ibibo. They gave the founder, Ashish Kashyap, $5 million dollars to grow ibibo. Using this money, Kashyap started 2 divisions of ibibo- Goibibo(the travel website) and ibibo pay(so that people can pay online on the Goibibo website).

In 2014, Kashyap sold Ibibo Pay to Prosus. At that time, Prosus already had a global fintech company called PayU. So they merged ibibo Pay with PayU to create a subsidiary called PayU India.

PayU India started as a payment gateway but has quickly expanded to other fintech areas like lending, mobile payments, etc.

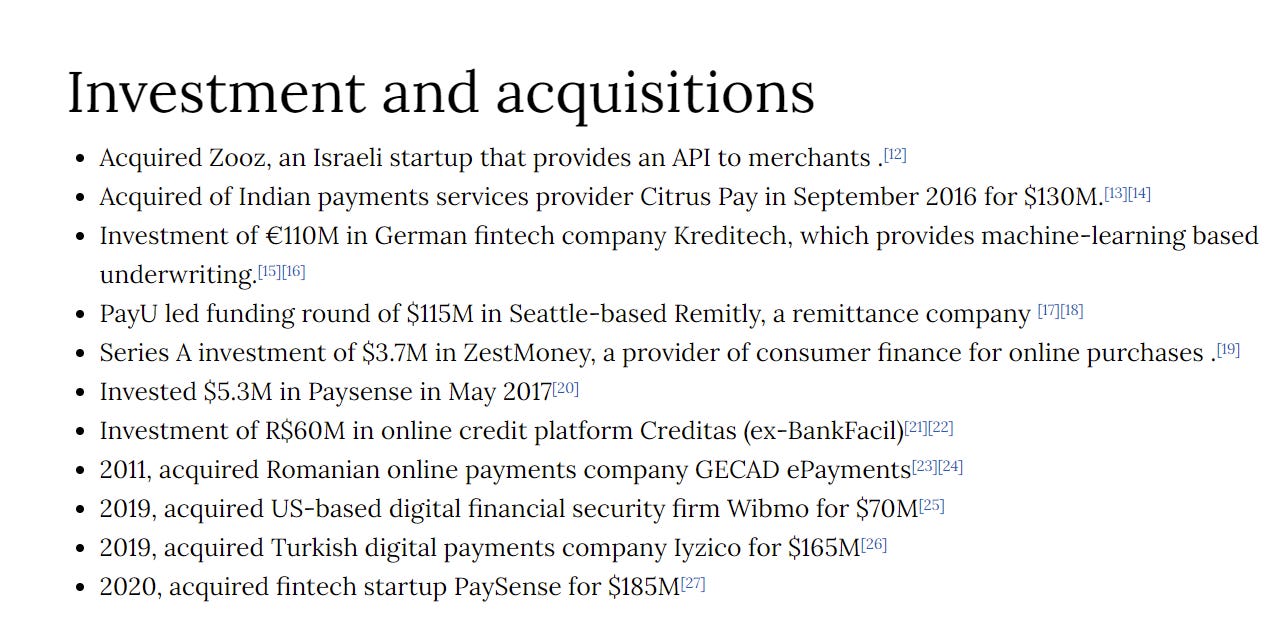

Here comes the interesting part- most companies build their own products, right? But PayU doesn’t. Remember Prosus had that money bag from Tencent? So Prosus gives this money to its companies to grow. The result? PayU simply acquired other companies to grow.

For example, Citrus Pay was PayU's rival in the payment gateway business. So PayU acquired it for $130 million in 2016. This was the biggest fintech acquisition at that time. PayU got rid of its competitor and got 30 million new customers.

In 2019, they acquired Paysense, a digital credit platform. Paysense used some ML/AI stuff to analyze customer's creditworthiness. By acquiring Paysense, PayU India entered the lending sector. And they acquired Wibimo, another fintech startup that provides security for online payments.

PayU has expanded all over the world using this strategy. I found a long list of acquisitions on their Wikipedia page:

Forbes has a nice name for this strategy: Buy. Build. Repeat.

PayU’s ‘buy, build, repeat’ playbook, reckon industry experts, has hastened its operations in India. Look at the revenue: From Rs 154 crore in FY15 to a staggering Rs 1,194 crore in FY20. Even the losses have dipped and stabilised: From a peak of Rs 249 crore in FY17 to Rs 99.5 crore in FY20.

Not to forget, PayU India is profitable :)

This completes the PayU side of the story. Now I'll take you to the Billdesk side.

🕹Online payments in India in the year 2000? Who does that?

These guys👇

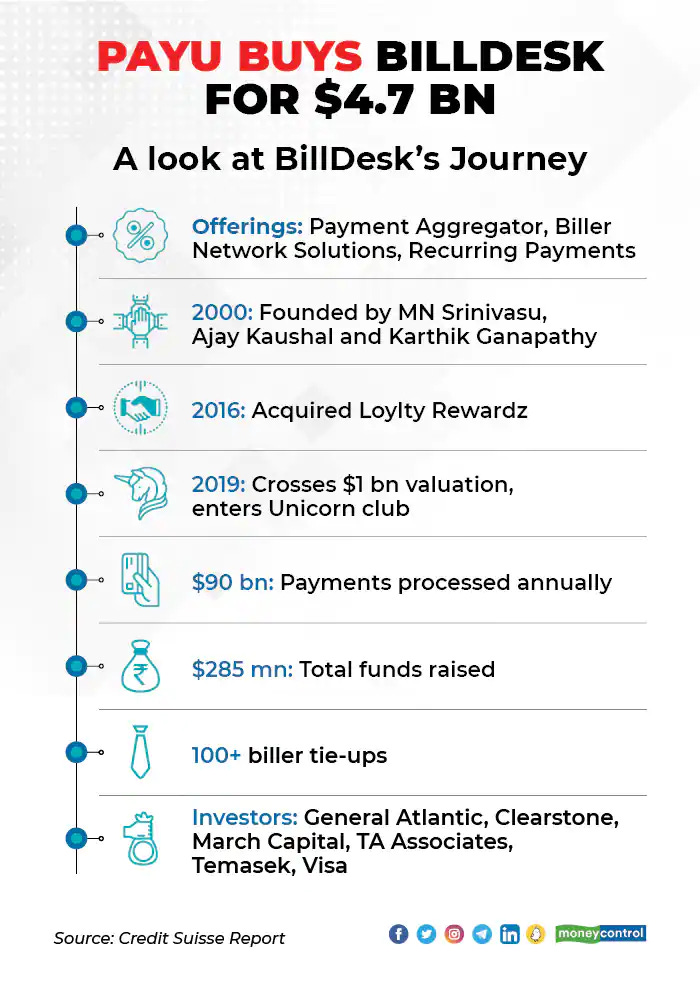

In the year 2000, MN Srinivasu, Karthik Ganapathy, and Ajay Kaushal left their jobs to start an online payment company called Billdesk (did we even have the internet at that time?????)

Billdesk started as a payment gateway-a tool through which merchants can accept payment from customers through credit cards, debit cards, UPI, net banking, etc etc. At that time, online payment meant credit card or debit card. UPI and net banking were yet to be invented.

This (probably) makes Billdesk the oldest payment gateway in our country.

I thought payment gateway must be some boring business, but I was amazed to see that Billdesk had so many competitors: TechProcess Payment Services, Razorpay, Airpay, Oxigen, PayUbiz, Paytm, Instamojo, CCAvenue, PhonePe, and Payworld!!! Even our local hero PayU was a competitor.

This is where Billdesk did big brein.

The customer base of most of their competitors was startups and tech companies. So Billdesk avoided all this competition by focusing on a very different customer base: govt institutions(like BSNL) and BFSI companies(BFSI= Banking, Financial service, and insurance. In simple language, banks, and insurance companies).

This was a smart move: these big institutions are a very lucrative market. Plus, Billdesk didn't have any competition here because convincing these institutions is very difficult.

The result of this big brein move? Billdesk processes $90 billion in payments per year and has a solid 60% market share in bill payments!! Plus, their expenses have kept decreasing while their profits have kept increasing🔥🔥🔥

🕹Now you know everything about PayU and Billdesk.

PayU is a fintech company that does payments, lending, etc. Instead of building a product itself, it just acquires another company. This helps in reducing competition. And PayU can expand to new markets without wasting time.

Billdesk is a fintech company that is a payment gateway and bill-payment platform. Billdesk has 60 percent of bill payments share and a big customer base of govt institutions(like BSNL) and BFSI companies.

🕹Now it's time to understand the reason behind the acquisition.

📌More competition, less growth

PayU has been facing a lot of competition from new startups like Razorpay. Razorpay has become the No.1 payment gateway and displaced PayU. To keep growing, PayU needed more customers. They could try to acquire new customers on their own. But remember what I told you earlier- PayU doesn't like to waste time in building things. It prefers to grow through acquisitions. Billdesk is a good choice: it has a huge customer base of Govt institutions and BFSI clients.

📌New market: Bill payments

I mean, this is not a new market. It's more like a subset of the payment gateway market. But it's a lucrative market with a lot of recurring revenue and Billdesk had established a 60% market share. So after buying Billdesk, PayU gets all this lucrative market.

📌The reality of payment business

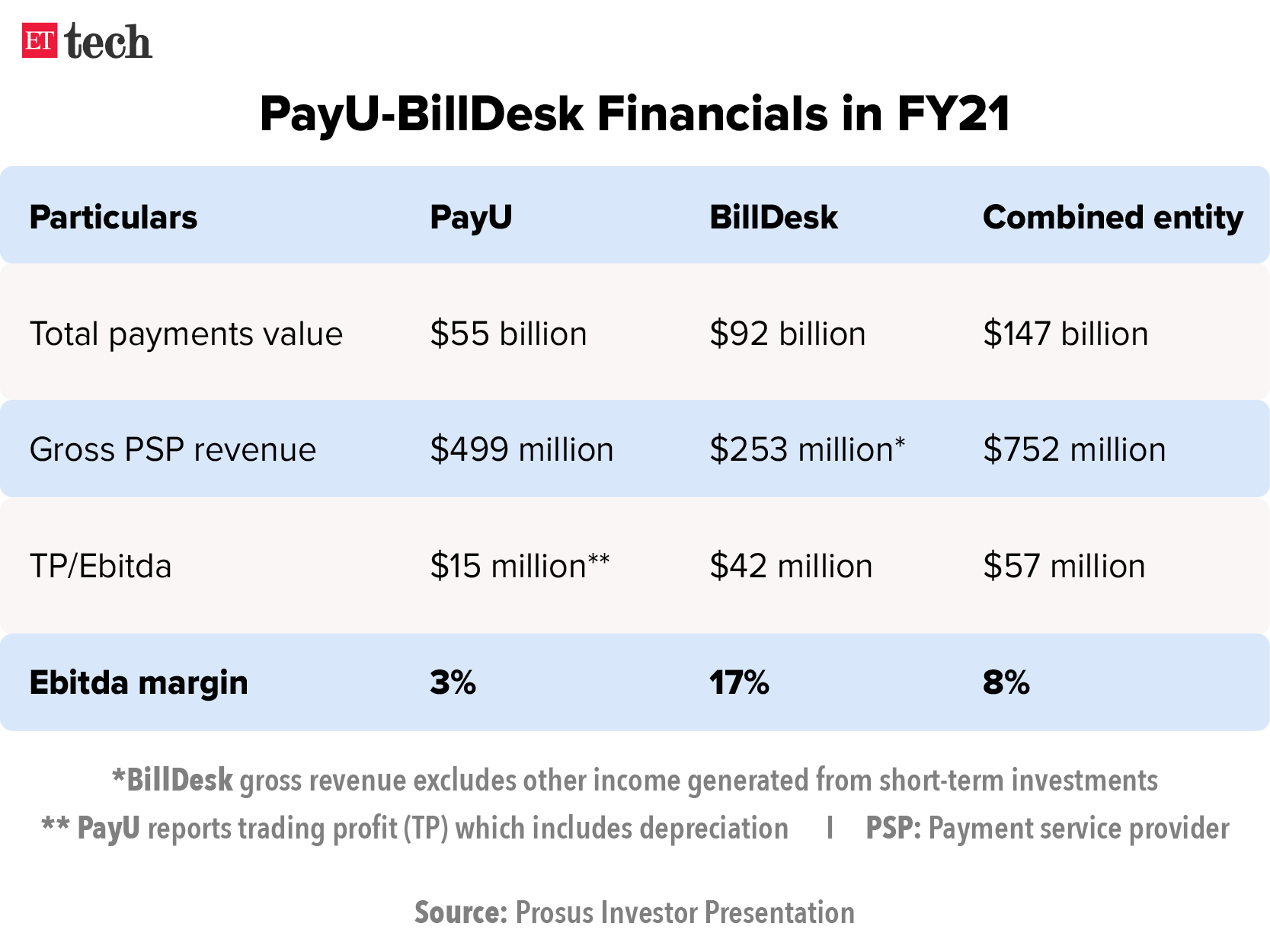

Payments are turning to be a bad business. Volumes are high but margins are low. Unless a company has a lot of customers, it won't be successful. That's why lots of payment companies are getting acquired into a few big companies. After the acquisition, PayU India and BillDesk will handle four billion transactions a year combined- four times PayU’s current size in India.

Plus, RBI is coming up with new rules for payment aggregators and payment gateways. RBI will now have more oversight on all these companies to make sure they are following the rules.

📌Indian fintech🚀🚀

Indian fintech is has a lot of potential. Huge population, under-served people, and huge scope of disruption are what make India a very attractive market for fintech players, especially on the payments side. PayU can possibly expand more deeply in lending, acquiring more fintechs to become a fintech giant. So in one way, this acquisition is a bet on this fast-growing sector. BCG says that Indian fintech will become a $150 billion market by 2025.

Also, India is becoming the new destination for global investors. Now that China has become anti-tech, India is seen as the next best market for fintech companies to exploit the gaps and solve for the existing gaps while scaling their own businesses. A win-win proposition for everyone, don't you think?

This wraps up today’s article.

Thanks to Yash Agarwal and Adwait Pisharody for their valuable contributions to today’s article.

If you enjoyed reading this article, please share it with your friends. I’m sure they will also find it informative.

And if you’re new here, please subscribe- you get weekly deep dives on Indian startups.

If I made a mistake or if you’d like to give feedback, please comment below.

Here are some insightful Twitter threads from this week:

Follow me on Twitter so that you don’t miss all these insights:

Thanks for being a supporter! Bye bye and have a great day!

Love reading your articles! The in-depth research is too good!

Just wanted to clarify a thing on the comment - "Now that China has become anti-tech, India is seen as the next best market for fintech companies to exploit the gaps"

China has not become anti-tech. They are just trying to strop the growth of monopolies and put curbs on industries such as after-school tutoring, gaming, etc and trying to improve regulations on data storage and sharing. By these measures, they are trying to make sure that Baba and Tencent do more for the community (middle-class and small businesses).

China is promoting tech in the "Greenspace" - carbon capture, electric vehicles, alternative energy and materials.

😮Interesting as always!!! 🔥🔥

Insightful 💡💡